Ebara Jitsugyo (6328)

Worth more without the business investors worry about

Good morning. Today’s company is Ebara Jitsugyo (6328), a public-sector water-infrastructure contractor with a hidden environmental-equipment business inside it.

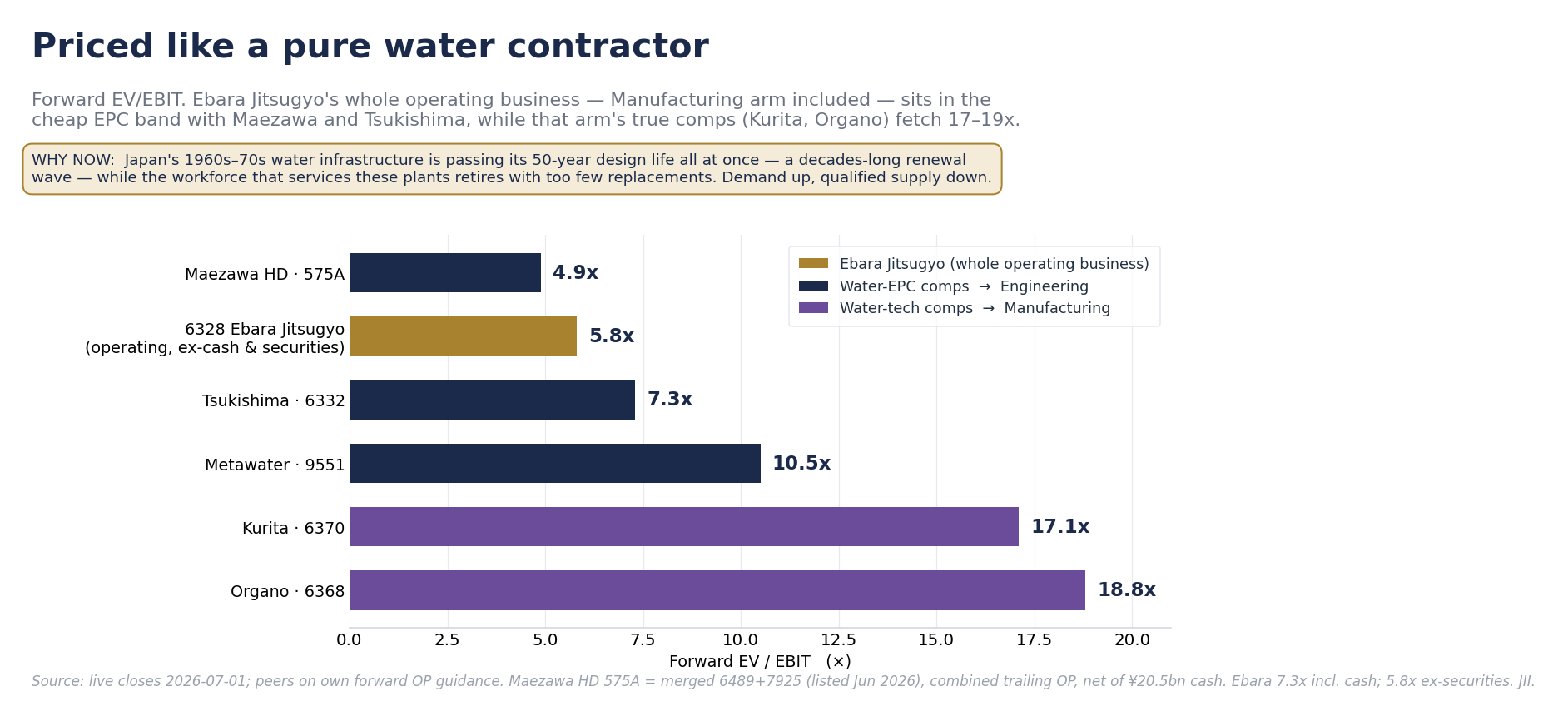

At a ¥58bn market cap, the stock trades at 7.3x forward EV/EBIT — among the cheapest of the listed Japanese water-infrastructure names, and priced like a plain EPC contractor even though the company runs a 15% operating margin, 22% ROCE, net cash, and a record order book.

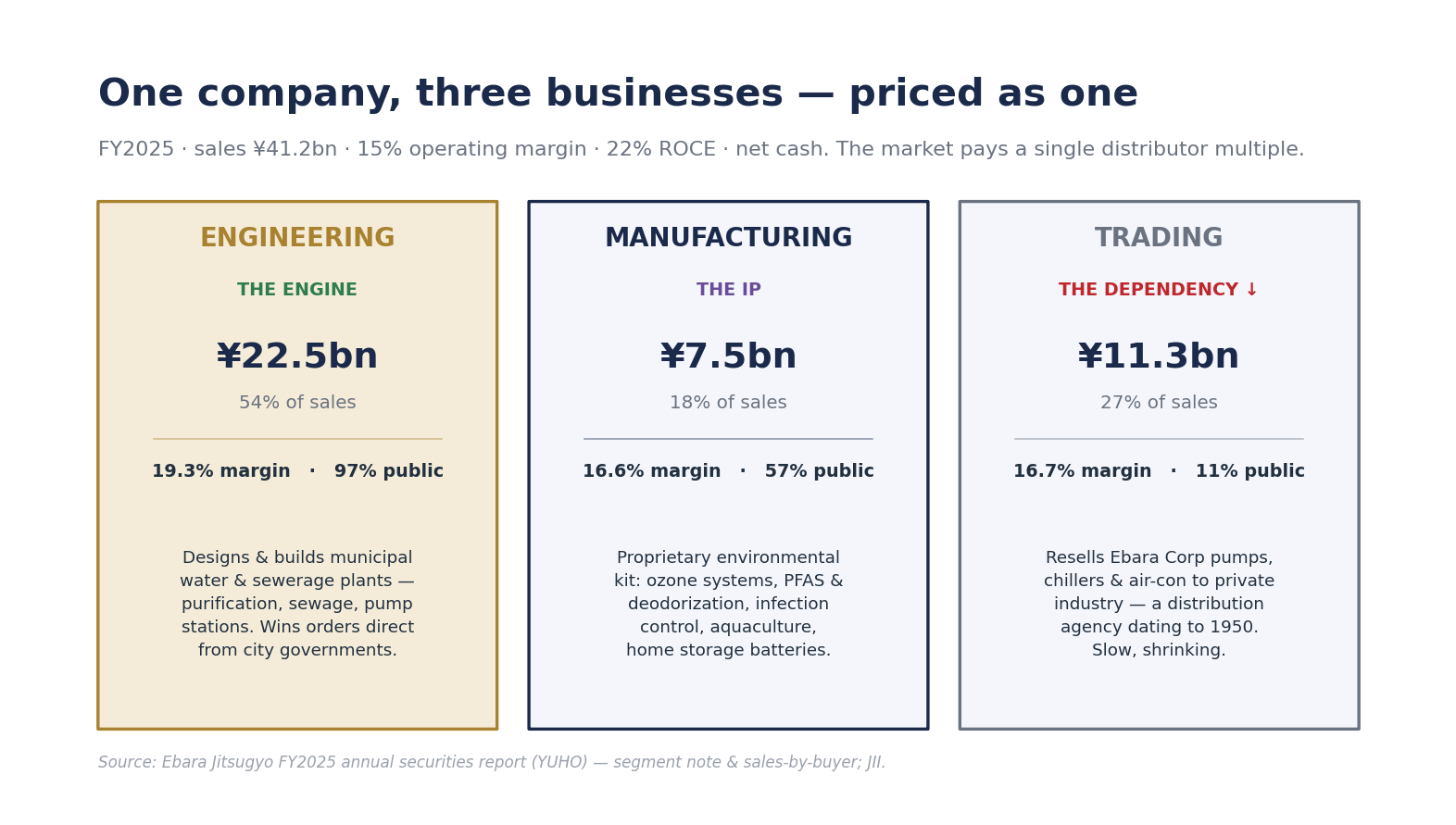

At first glance, Ebara Jitsugyo looks like a cheap, Ebara-dependent contractor. That is the problem. The company is actually three businesses under one roof.

Engineering is the core business. It accounts for 54% of sales. It designs and builds municipal water and sewerage facilities, including purification plants, sewage treatment facilities, and pump stations. It wins orders directly from city governments. The segment has a 19% margin and 97% of sales come from the public sector.

Manufacturing accounts for 18% of sales. It makes Ebara Jitsugyo’s own environmental equipment, including ozone systems, PFAS treatment equipment, deodorization equipment, infection-control systems, aquaculture facilities, and home storage batteries.

Trading accounts for 27% of sales. It resells Ebara Corporation (6361) pumps, chillers, and air-conditioning equipment to private-sector customers. This distribution relationship dates back to 1950.

These are three different businesses, selling to three different customer groups. But the market lumps them together and prices the whole thing like a single low-end contractor.

That is the mispricing. Investors see the Ebara name, the Ebara Corporation distribution business, and Ebara Jitsugyo’s large holding in Ebara Corporation shares. So they never look past the Ebara link, and the whole company gets a plain contractor multiple — with no credit for the Manufacturing arm or the balance sheet.

But the Ebara-linked business is now the smallest, slowest, and shrinking part of the group. If you separate it out and value the Engineering and Manufacturing businesses against their real peers, the company is worth more than today’s share price.

1. Why now: Japan’s water infrastructure needs rebuilding

Japan built much of its modern sewerage and water infrastructure during the high-growth decades from the late 1960s onward. That stock is now aging together, creating a long renewal cycle just as local governments lose the experienced engineers and operators needed to maintain it (see MLIT guideline).

So demand is rising, while qualified supply is becoming harder to find. That is good for companies with the licenses, engineers, and project track record to do this work.

Ebara Jitsugyo is built for this kind of market. Its Engineering arm has 378 certified engineers, including construction-management and professional engineers, out of a workforce of about 610. A new entrant cannot build that overnight.

Ebara Jitsugyo’s Engineering business should be compared with listed water-EPC contractors such as Tsukishima (6332), Metawater (9551), and Maezawa (575A). These trade at roughly 6–11x forward EV/EBIT.

Its Manufacturing business should be compared with higher-rated water-technology companies such as Kurita (6370) and Organo (6368). These trade at roughly 17–19x.

Yet Ebara Jitsugyo’s whole operating business trades at just 5.8x forward core EV/EBIT (after removing cash and securities) — near the low end of that EPC range, even though nearly a fifth of it is the higher-multiple Manufacturing business.

In effect, the market is applying a plain EPC-contractor multiple to the entire company. Investors pay a contractor price for the Engineering business and get the higher-quality Manufacturing business — whose closest peers trade at 17–19x — almost for free.

2. Why the stock is cheap: Trading and the Ebara Corporation stake

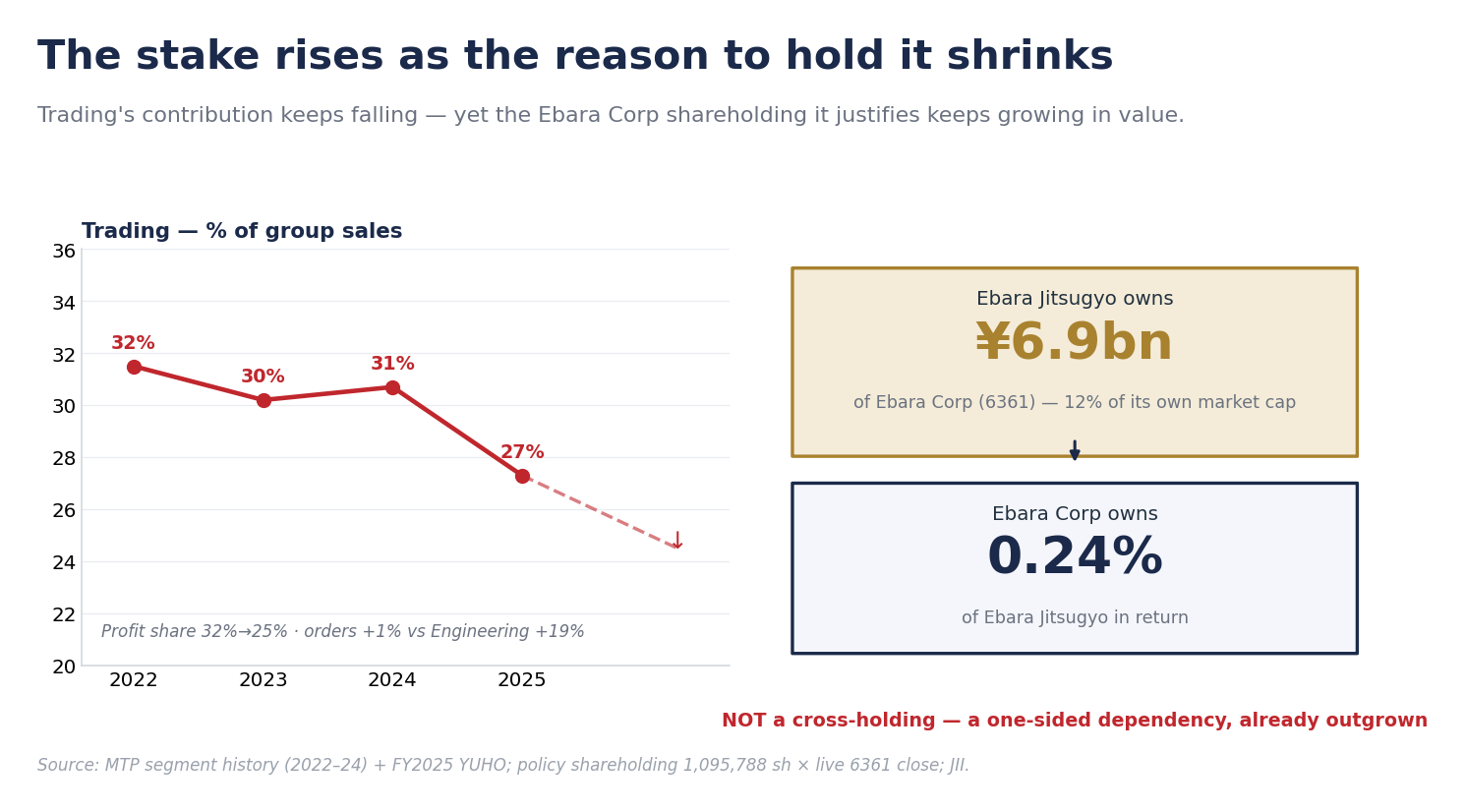

The main drag is the Trading business and the shareholding tied to it.

Ebara Jitsugyo owns 1,095,788 shares of Ebara Corporation. That stake is worth about ¥6.9bn, or 12% of Ebara Jitsugyo’s own market cap.

The company says it holds these shares to maintain and strengthen the distribution relationship with Ebara Corporation.

But there is a contradiction. The Ebara Corporation stake keeps rising in value, while the business relationship it is meant to protect keeps becoming less important.

Trading is already fading. Since 2022, its share of group sales has fallen from 31% to 27%, and its share of segment profit has dropped from 32% to 25%. Over the same period, Engineering’s profit share has risen from 44% to 58%.

FY2025 widened the gap. Engineering orders rose 18.8%, sales rose 19.0%, and profit jumped 76.8%. Trading orders rose only 1.1%, sales fell 2.3%, and profit rose 7.6%. Engineering also ended the year with a ¥25.1bn backlog, up 8.2%. If that backlog converts, Trading should keep shrinking as a share of the group.

This is not even a balanced cross-shareholding. Ebara Corporation owns only 0.24% of Ebara Jitsugyo in return.

So Ebara Jitsugyo is carrying a one-sided dependency that it has already outgrown.

3. The catalyst: NAVF is already pushing

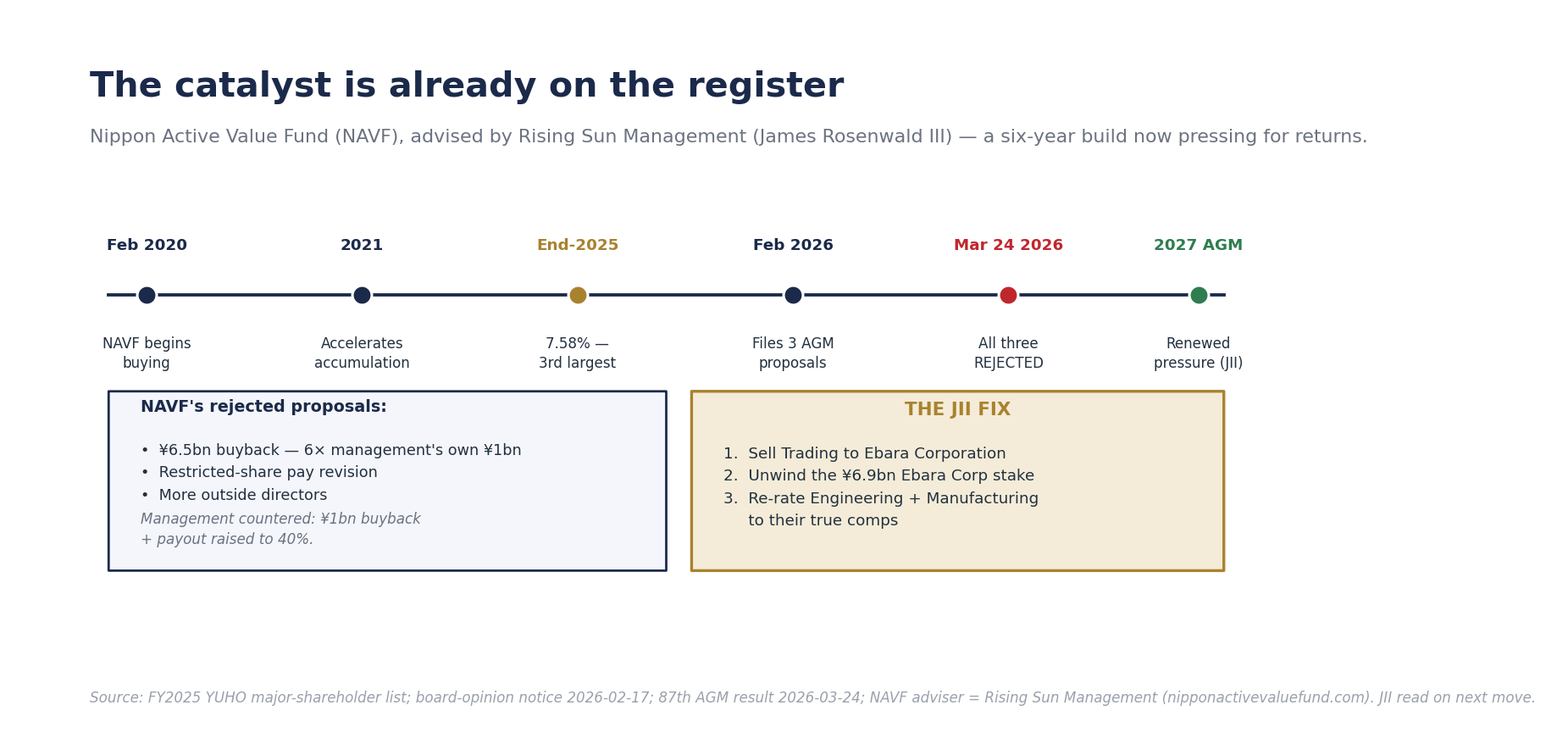

The catalyst is already on the shareholder register.

Nippon Active Value Fund, advised by activist adviser Rising Sun Management, first appeared as a 5%+ holder in the large-shareholding filings in 2021. Since then, its role has shifted from accumulation to open engagement.

The latest large-shareholding change report, filed in June 2026, shows a NAVF-led joint-holder group owning 10.65%.

That makes NAVF more than a passive shareholder. In February 2026, NAVF submitted three proposals for the March AGM:

a ¥6.5bn buyback

a revision to restricted-share compensation

more outside directors

The buyback proposal was six times larger than management’s own ¥1bn buyback plan.

All three proposals were rejected on March 24. Management responded with a ¥1bn buyback and raised the payout ratio to 40%.

NAVF is still the live catalyst. Its proposals failed, but management still responded with a higher payout ratio and a buyback.

That means the debate has started. With NAVF still on the register, the next question is not just how much cash Ebara Jitsugyo returns, but what assets it should keep.

The cleaner fix: sell Trading to Ebara Corporation

The clean solution is simple: sell the Trading business to Ebara Corporation.

Ebara Corporation would bring the distribution margin in-house. Ebara Jitsugyo could still source Ebara equipment when needed for its Engineering and Manufacturing projects, but it would no longer need to carry the dependency.

It would also no longer need to hold the ¥6.9bn Ebara Corporation stake.

That would leave Ebara Jitsugyo as a cleaner Engineering and Manufacturing infrastructure company, with a much simpler investment case.

The clean-up math has three parts.

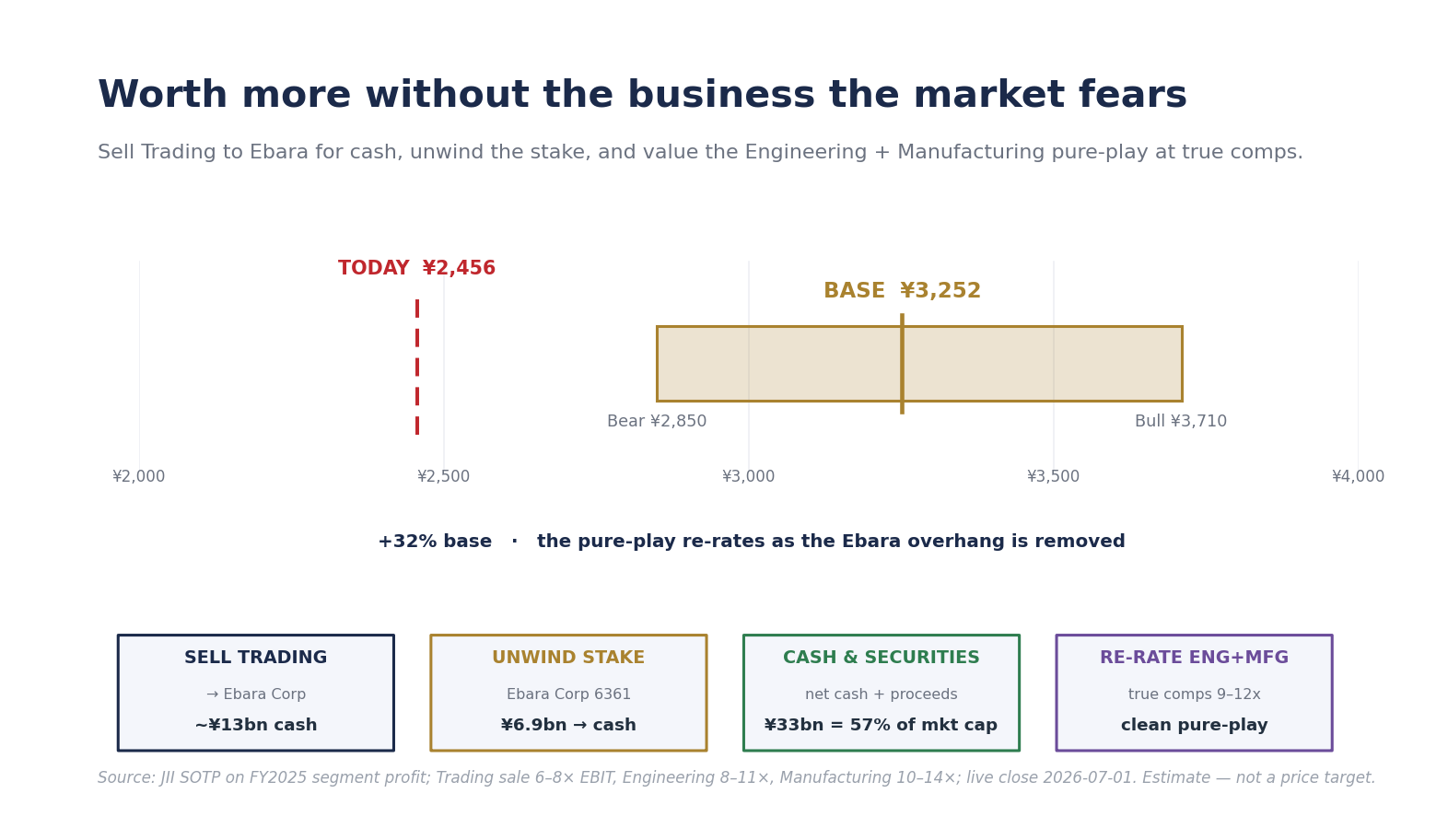

First, sell Trading. It earned ¥1.88bn in FY2025 segment profit. At a 7x distributor multiple, that business is worth about ¥13bn. Ebara Corporation is the logical buyer because it could bring the distribution margin back in-house.

Second, sell the Ebara Corporation shares. Ebara Jitsugyo owns 1,095,788 shares, worth about ¥6.9bn at ¥6,300 per share.

Third, value the remaining business. Engineering and Manufacturing earned about ¥4.2bn after head-office costs. We value them at about ¥44bn, or roughly 10x profit, reflecting Engineering’s public-sector backlog and Manufacturing’s proprietary environmental equipment.

Add it up: ¥44bn for the core business, ¥13bn from selling Trading, ¥12.4bn of net cash, about ¥7bn from securities, and ¥0.6bn of investment property. That gives ¥77bn of equity value, or about ¥3,250 per share. That is roughly one-third above today’s ¥2,456 share price.

The point is simple: Ebara Jitsugyo is worth more without Trading. Selling it would turn the market’s biggest concern into cash and let investors value Engineering and Manufacturing on their own merits.

Full profile: https://jpinv.com/en/compounders/6328/

Related links:

Methodology: https://jpinv.com/en/compounders/methodology/

Watch universe: https://jpinv.com/en/compounders/universe/

All compounder profiles: https://jpinv.com/en/compounders/profiles/

Capital allocation signals feed: https://jpinv.com/en/compounders/feed/

Parting Ways with JII Compounders

We are changing what we look for.

Until now, JII Compounders focused mainly on cheap compounders, especially software names with high revenue growth and strong margins. But many of those stocks have continued to fall, and AI may be hurting some of them in ways we have not modeled well enough.

Rather than guessing how AI will change software, we want to focus on companies where the demand picture is clearer. Ebara Jitsugyo is a good example: it is not a classic software-style compounder, but it is cheap, and it benefits from visible demand for water-infrastructure renewal and environmental regulation.

Going forward, our screen will be looser, but our conviction bar will be higher. Ebara Jitsugyo is my highest-conviction idea in Japanese water infrastructure.

Next, I plan to look at food trays. Prices have been rising, and I think there are structural reasons why demand can keep growing while producers still have room to raise prices.